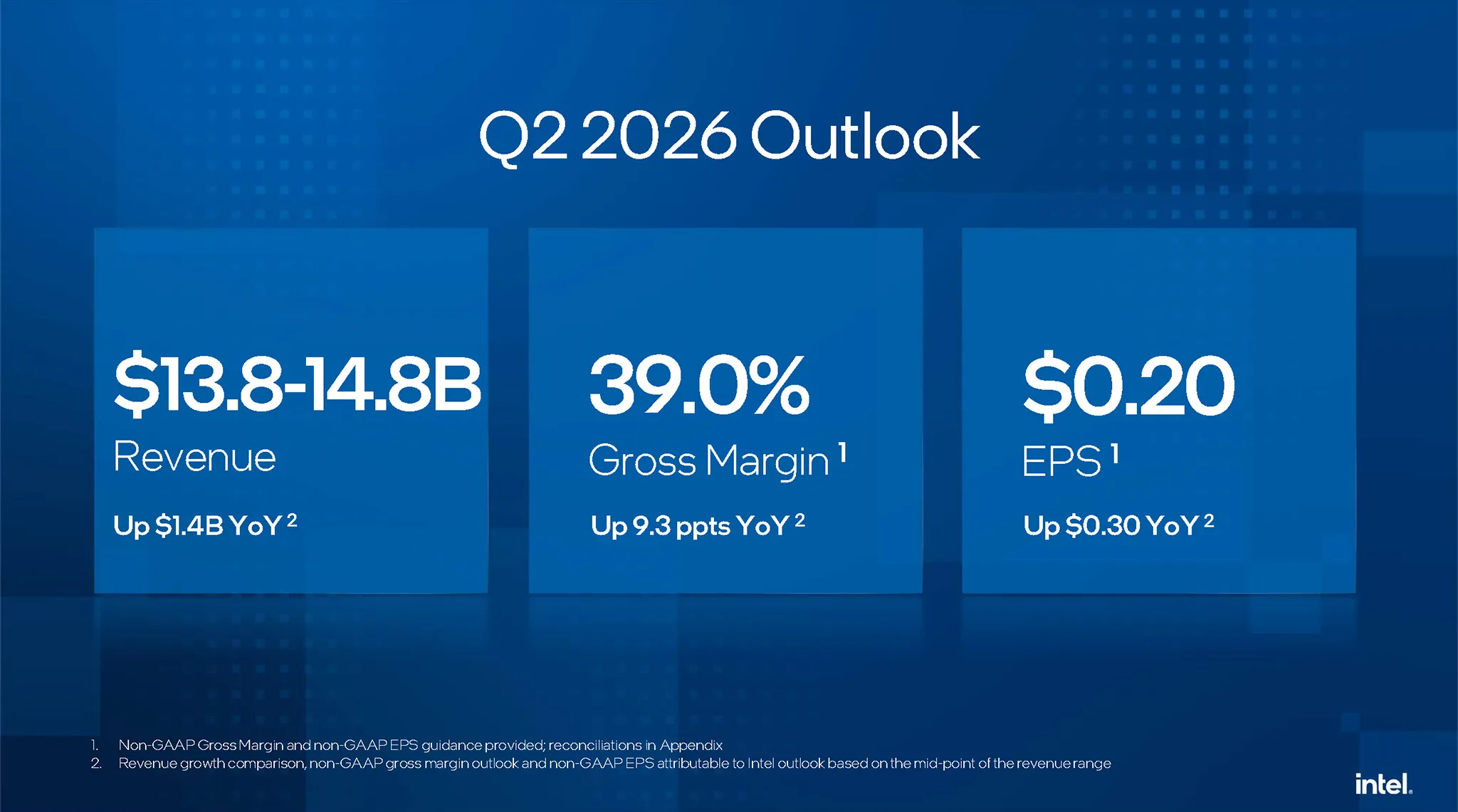

Intel Q1 2026 earnings: From survival to acceleration in the AI era

Intel has a golden opportunity to reclaim the throne, fueled by the Agentic AI wave and impressive strides with its 14A node.

- Revenue hit $13.577 billion (up 7% YoY) with a 41% gross margin, driven by strong pricing power and the unexpected success of the 18A process.

- The report shows a massive GAAP net loss of $3.728 billion, largely due to a non-cash goodwill impairment charge for Mobileye; however, core operational profit (non-GAAP) remains solidly in the black.

- The Agentic AI trend is shifting the CPU-to-GPU deployment ratio in AI servers from 1:8 down to 1:4 (and trending toward 1:1), leading to record CPU shortages and price hikes.

- The "Terafab" mega-project leverages the Intel 14A node to build the world's largest AI chip foundry complex, aiming for 1 Terawatt of compute capacity.

- Intel still faces AMD's "market skimming" strategy in the premium server segment, alongside severe supply chain threats stemming from Middle East conflicts.

Article content

Intel Q1 2026 financial overview

Closing out Q1 2026 (ending March 28, 2026), Intel marked its sixth consecutive quarter beating Wall Street's revenue estimates. However, the glaring delta between standard accounting figures (GAAP) and adjusted metrics (non-GAAP) highlights the massive turbulence of a titan still in the midst of a business model pivot.

Revenue and margin expansion

Intel posted net revenues of $13.577 billion, a 7% year-over-year (YoY) increase. This is a critical indicator that Intel's grueling efforts to defend core market share and tap into the AI gold rush are finally bearing fruit. CEO Lip-Bu Tan and CFO Dave Zinsner pointed to this as proof of solid execution across the company's entire ecosystem.

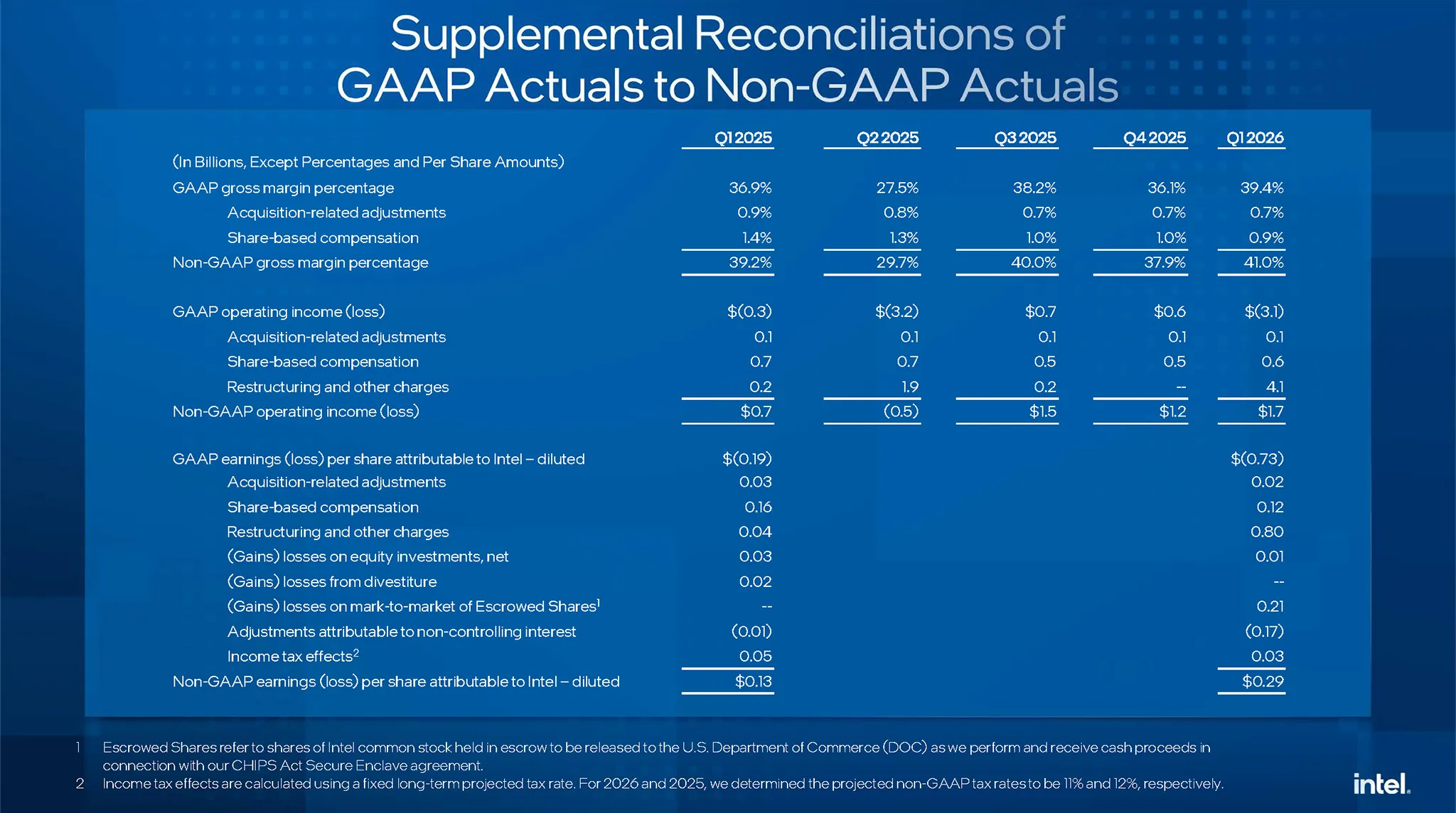

Not only is Intel moving more silicon, but they're also making more money per chip thanks to expanding gross margins. On a GAAP basis, gross margin hit 39.4% (up 2.5% YoY). More impressively, non-GAAP gross margin (excluding one-off charges) touched 41% - crushing management's guidance by 6.5 points and up 1.8% from Q1 2025. Three main drivers fueled this upside:

- Pricing Power: Intel proactively adjusted its pricing to match market demand, effectively offsetting escalating input costs.

- Premium Mix: A surge in higher-margin, high-end chip sales across both client computing and data center segments.

- The 18A Node is Yielding: Defect densities and yield rates for the Intel 18A process are far better than expected. Keeping yields high during the early production ramp has saved Intel from a massive chunk of depreciation costs.

A massive accounting loss

Despite the pretty revenue and margin top-lines, Intel's GAAP net income cratered to a colossal $3.728 billion loss (an EPS of -$0.73) - significantly worse than the $821 million loss from the same quarter last year. Why the paradox?

The primary culprit is a bloated "Restructuring and other charges" line item totaling $4.070 billion. Per the 10-Q filing, $3.965 billion of this is actually a non-cash goodwill impairment charge tied to its autonomous driving subsidiary, Mobileye. Mobileye's plunging market cap, compounded by macroeconomic headwinds and escalating geopolitical tensions in the Middle East (its primary base of operations), triggered the write-down. Using an income approach for valuation, Intel had to apply a higher discount rate to reflect these new market risks, effectively slashing future expected cash flows. This resulted in a massive paper loss, evaporating Mobileye's goodwill value from $8.2 billion down to $4.3 billion.

Additionally, Intel recorded $74 million in severance costs tied to its "2025 Restructuring Plan" aimed at streamlining operations and refocusing resources. On the bright side, this belt-tightening and headcount optimization drove R&D and MG&A (Marketing, General, and Administrative) expenses down by 7% and 12% respectively, amplified by the divestiture of Altera in Q3 2025.

That nearly $4 billion Mobileye loss is strictly on paper, which is why the non-GAAP figures paint a much more accurate picture of Intel's actual health. Stripping out the anomalies, non-GAAP operating income came in at $1.668 billion, with net income hitting $1.485 billion (EPS of $0.29). That $0.29 EPS is a massive 123% jump from last year's $0.13, completely obliterating previous break-even forecasts. This non-GAAP profitability is a firm indicator that Intel's core semiconductor manufacturing and design business is still a reliable cash cow.

GAAP (Generally Accepted Accounting Principles) is the strict, standardized accounting rulebook that requires everything to be recorded. For example, when subsidiary Mobileye's market value dropped, GAAP forced Intel to book it as a loss (goodwill impairment) even though no actual cash left Intel's bank accounts. Non-GAAP, on the other hand, is an adjusted metric calculated by the company that strips out these paper losses and one-time restructuring costs. Looking at the non-GAAP numbers reveals that Intel's core business operations are still turning a healthy profit ($1.485 billion this quarter).

Finally, the finance division recorded a $1.09 billion mark-to-market loss due to the revaluation of Escrowed Shares tied to the US Government's CHIPS Act funding. However, this was partially offset by a $223 million reversal from reduced indemnification obligations related to the SCIP manufacturing project in Ireland.

A mark-to-market loss is an accounting quirk. To receive CHIPS Act funding, Intel had to commit to holding a block of escrowed shares (collateral shares that cannot be traded). When Intel's market stock price increases, the value of this collateral also increases. Under accounting rules, this revaluation discrepancy forces Intel to record it on the books as an unrealized loss, totaling $1.09 billion in this case. It's just spreadsheet math - Intel didn't actually burn a single cent of real cash.

Segment-by-segment breakdown

Under the new financial model introduced in 2024, Intel has strictly decoupled the financials of its product groups (Intel Products) from its manufacturing arm (Intel Foundry). The goal is crystal clear: provide cash flow transparency, force the individual units to be fiercely competitive, and show investors the true, eye-watering cost of staying in the leading-edge node race.

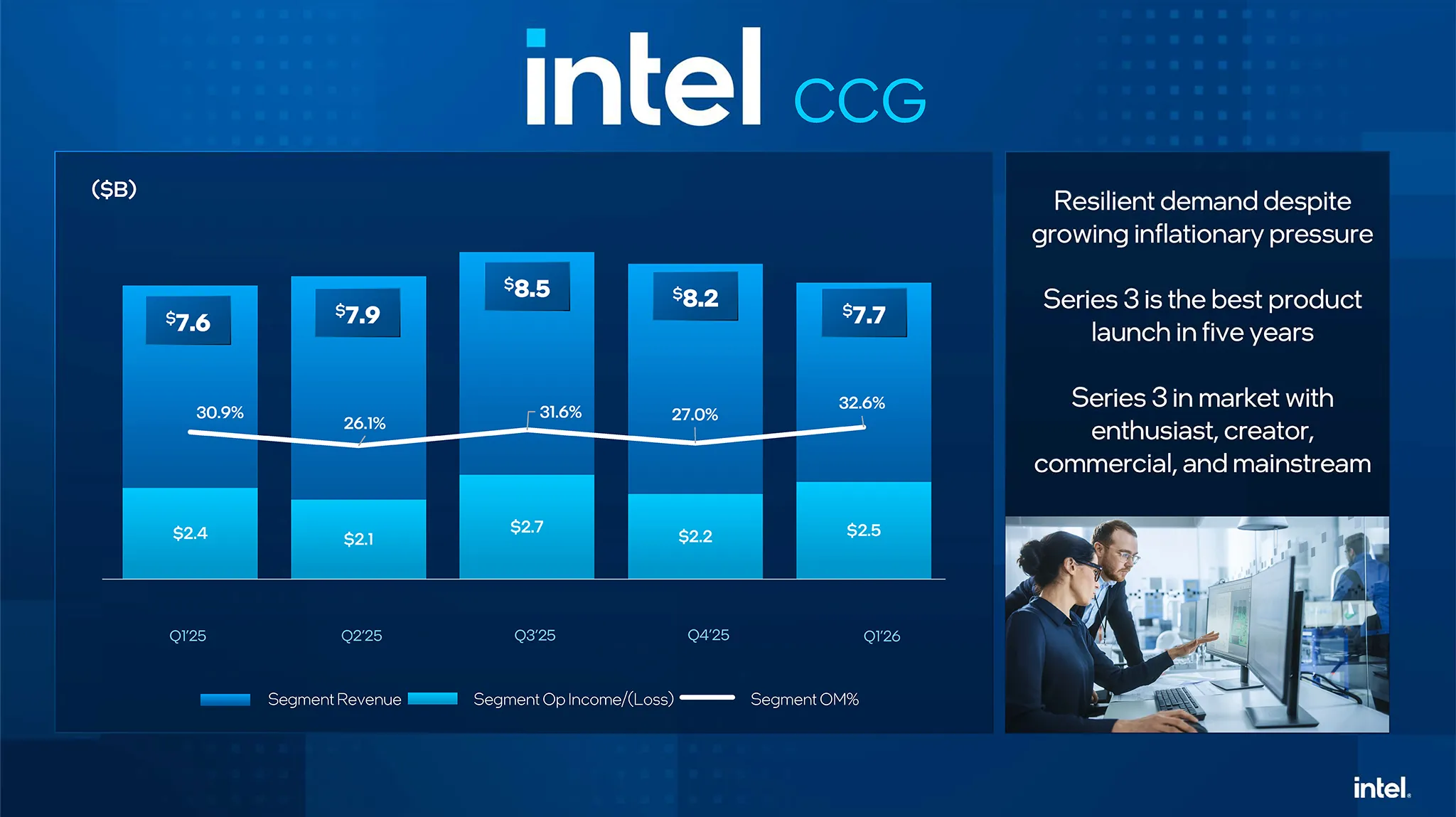

Client Computing Group (CCG)

Often viewed as Intel's traditional cash cow, CCG hauled in $7.727 billion in Q1 2026 revenue. While that's only a modest 1% bump YoY, operating income jumped by $155 million (hitting $2.516 billion), maintaining a healthy 33% operating margin.

The real story behind that modest 1% growth is a massive qualitative shift in the sales mix. Average Selling Prices (ASPs) skyrocketed by 16%, driven by a hard push into the premium segment and proactive price hikes to offset costs. The standout here is the AI PC segment, which grew 8% sequentially and now accounts for over 60% of Intel's total client CPU mix.

However, unit volume actually dropped by 13%. Crucially, this wasn't a demand issue, but a supply constraint problem. The sheer demand for Core Ultra Series 3 and vPro chips essentially broke the supply chain. Intel admits that substrate and memory bottlenecks will likely persist through the first half of 2026. To alleviate this, Intel is accelerating its 18A ramp, most notably for the mainstream-targeted Core Series 3 processors, which feature new IP blocks and significantly improved battery life. CFO Dave Zinsner didn't mince words, calling the Core Series 3 launch CCG's strongest product rollout in five years.

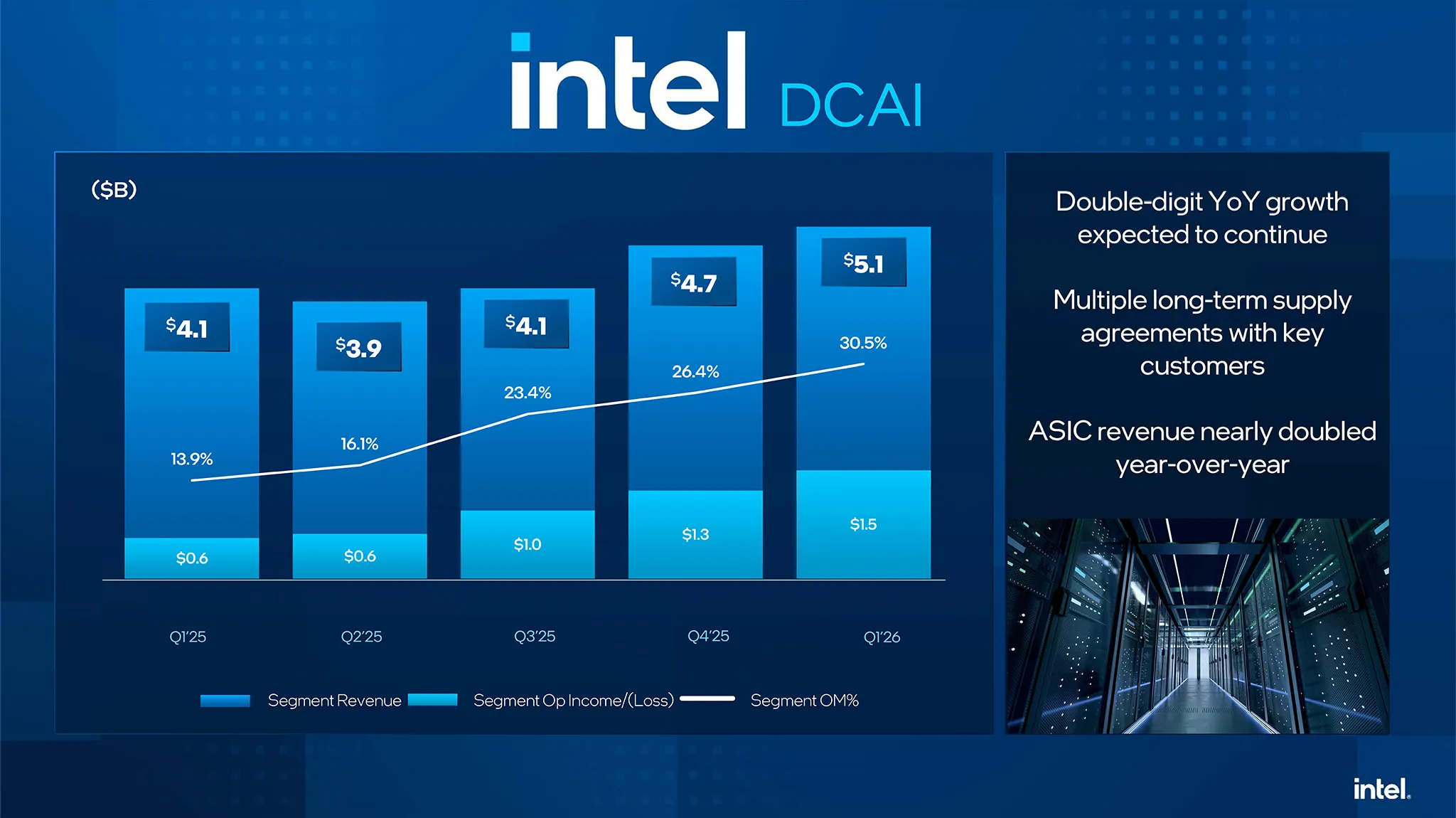

Data Center and AI (DCAI)

While CCG maintained the baseline, DCAI was the absolute star of the show. The division raked in $5.052 billion - a massive 22% YoY breakout. Better yet, operating income nearly tripled (from $575 million to $1.542 billion), dragging margins up from 14% to a stellar 31%.

Mirroring the client side, server CPU ASPs surged by 27%. Despite a 5% drop in volume due to capacity bottlenecks, the insatiable thirst for AI infrastructure handed Intel absolute pricing power over every wafer leaving the fab. ASIC (custom silicon) revenue also jumped over 30% sequentially, while networking gear pulled in $935 million.

DCAI's market position was further cemented by blockbuster partnerships. They inked a long-term deal with Google Cloud to deploy Xeon 6 processors and co-develop custom Infrastructure Processing Units (IPUs); they also teamed up with SambaNova to build a cross-platform AI inference architecture combining SambaNova's Reconfigurable Dataflow Units (RDUs) with Intel Xeon 6 CPUs. But the biggest flex? Archrival NVIDIA chose Xeon 6 as the host CPU for its DGX Rubin NVL8 supercomputers. It’s a loud reminder that the x86 architecture remains the undisputed king of system orchestration in heavy-duty AI infrastructure.

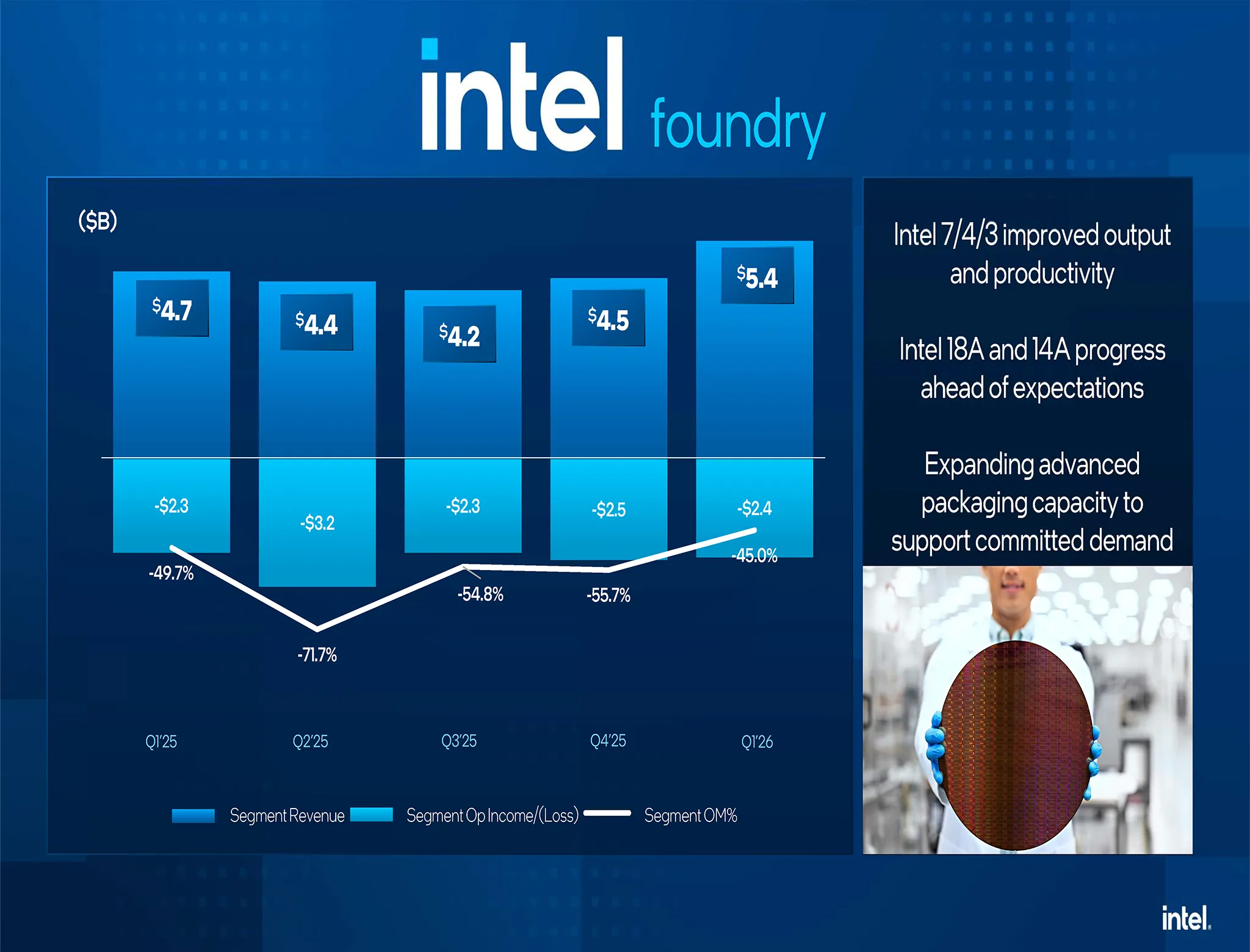

Intel Foundry

Billed as the trump card to dethrone TSMC, Intel Foundry reported $5.421 billion in revenue (up 16%). However, let's be real: $5.2 billion of that is essentially moving money from the left pocket to the right (internal revenue from fabricating wafers for CCG and DCAI). True external foundry revenue sits at a meager $174 million, and a good chunk of that increase is just an accounting side-effect of spinning off Altera (which is now classified as an independent customer).

On the bottom line, Intel Foundry remains a capital-incinerating black hole. It posted an operating loss of $2.437 billion (a -45% operating margin), although this is a $72 million improvement over Q4 2025. The bleeding is largely driven by massive depreciation burdens tied to the early production runs of the 18A node, compounded by eye-watering investments in Extreme Ultraviolet (EUV) lithography systems for the upcoming 14A process.

Still, leadership views this as the mandatory entry fee to stay ahead of the curve. On the upside, the backlog for advanced packaging services is growing. Intel also just announced fresh capital injections to expand its back-end test and advanced packaging facilities in Penang, Malaysia, prepping for an expected commercial boom in 2027.

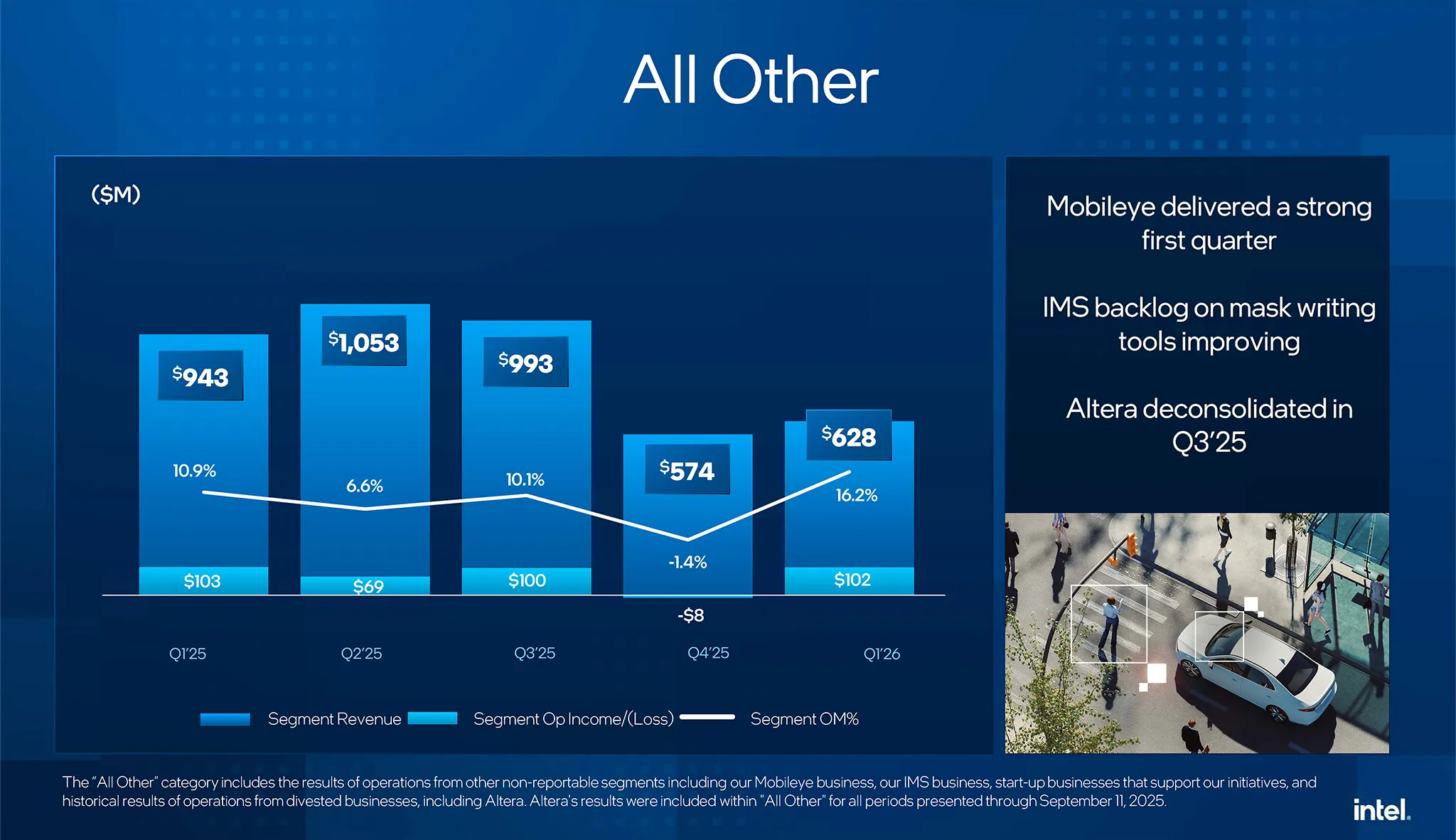

All Other

The "All Other" group brought in $628 million, a steep $315 million drop YoY. This decline is entirely expected, as Intel no longer consolidates the financials of the FPGA maker Altera (having sold a 51% stake to Silver Lake Partners in September 2025).

However, looking at it in isolation, the autonomous driving company Mobileye actually had an excellent cash-flow quarter. Mobileye's revenue hit $558 million (up $120 million YoY), driven by a strong recovery in demand for its EyeQ driver-assistance systems. Notably, Mobileye just dropped $637 million to acquire Mentee Robotics (an AI humanoid robotics startup) on February 3, 2026. This investment didn't just add $498 million in goodwill and $128 million in intangible assets to Intel's books; it signals a serious ambition to push deep into the massive physical automation market. The multi-beam mask writer business at IMS Nanofabrication (another unit in this group) is also showing a healthier backlog.

The view from the top

The Q1 2026 earnings call radiated an unprecedented level of confidence from CEO Lip-Bu Tan and CFO Dave Zinsner. After a grueling stretch of Wall Street skepticism and technical roadblocks, Intel is genuinely transforming. According to Tan, the company is undergoing a deep cultural reset: getting back to core engineering roots, becoming ruthlessly data-driven, and reviving the legendary "paranoid" spirit coined by former CEO Andy Grove (Only the Paranoid Survive).

Agentic AI: CPUs are cool again

The most fascinating thesis pitched by leadership is a structural shift in AI workloads. Phase one was all about GPUs training foundational models - a playground where NVIDIA held an absolute monopoly. But the AI world is shifting into practical deployment: Agentic AI, Edge AI, and robotics control. As AI transitions from brute-force training to inference, where systems must constantly process complex, branching logic paths, the CPU is no longer playing second fiddle. Management asserts that the CPU is reclaiming the throne as the central orchestration layer for the entire AI stack.

Think of standard AI as a super-smart encyclopedia - you ask a question, you get an answer. Agentic AI, however, is like an actual assistant. It doesn't just answer; it makes decisions, autonomously runs software, plans ahead, and independently executes workflows to complete the tasks you assign. This heavy logic requirement is exactly why future server arrays are thirsting for Intel CPUs to orchestrate these AI agents.

CFO Dave Zinsner highlighted a staggering reality: the CPU-to-GPU deployment ratio in AI servers is shrinking fast. From the early days of 1 CPU for every 8 GPUs (1:8), the ratio has now compressed to 1:4 (effectively doubling the number of CPUs required). Looking ahead at future Agentic AI deployments, this ratio is trending toward 1:1, or scenarios where the CPU might even become the dominant hardware.

This sudden spike in demand, slamming into supply chain walls, has turned Intel server CPUs into unobtainium. Lead times currently stretch out to six months, and prices have spiked by 20%. The revenue left on the table due to product shortages is in the billions (Zinsner literally noted the shortfall "starts with a B"), prompting the CFO to proudly declare: "CPUs are cool again."

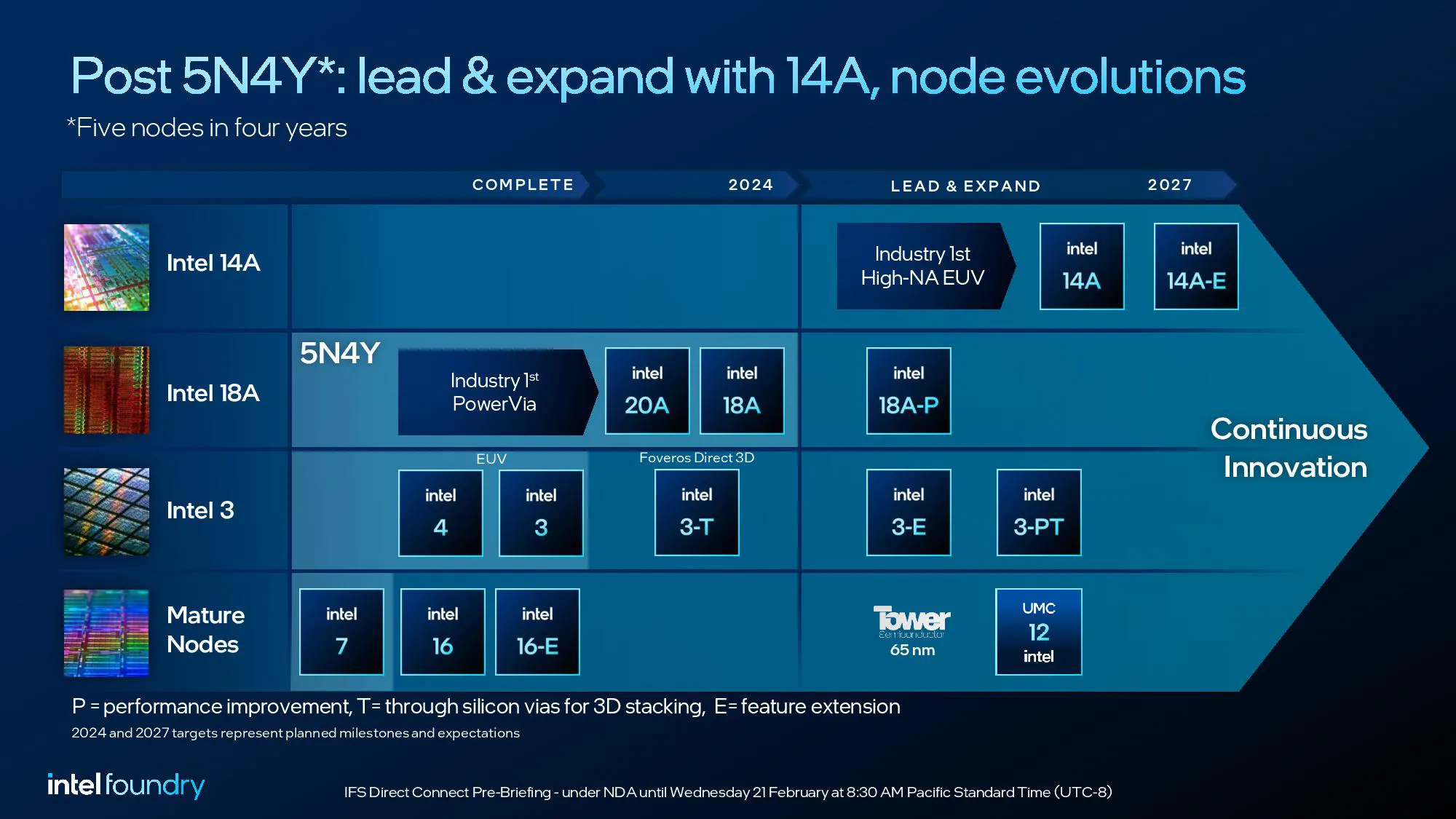

The unexpected performance of Intel 14A

Intel's swagger is further backed by a node roadmap that is executing almost unbelievably smoothly. The 18A process has officially entered its volume ramp, boasting yield rates that crush even the most optimistic internal projections.

But the real jaw-dropper is the next generation: the Intel 14A node. CEO Lip-Bu Tan revealed that 14A's maturity and performance are currently outpacing where 18A was at the same stage of development. Riding this rapid momentum, Intel is rushing to finalize the Process Design Kit (PDK) for 14A and expects to lock in commercial orders from major partners by the end of 2026. Furthermore, amid a severe global shortage in leading-edge wafer capacity, Intel is confidently migrating many of its own internal chip designs straight to 14A to guarantee supply chain autonomy.

The Terafab mega-project

Intel's ambition to conquer the foundry space is perfectly encapsulated by "Terafab" - a strategic mega-project built in partnership with Elon Musk's empire (SpaceX, xAI, Tesla).

Located in Texas, Terafab isn't just a standard fab; it's a manufacturing complex targeting an insane 1 Terawatt (TW) of AI compute capacity annually. To call this ambitious is an understatement: Terafab's planned scale is roughly 50 times the current combined capacity of TSMC, Samsung, and Intel (which currently hovers around 20 Gigawatts). The project aims to fundamentally refactor silicon fabrication, leveraging non-traditional automation solutions to exponentially increase manufacturing efficiency and solve the global AI supply bottleneck.

Elon Musk himself revealed that Terafab will directly utilize the Intel 14A process to mass-produce AI5 inference chips for self-driving cars, Optimus robots, and ultra-durable silicon for SpaceX's orbital data centers. Having a notoriously demanding billionaire like Musk bet his hardware future on 14A (instead of TSMC) is a priceless endorsement. It proves that Intel's Integrated Device Manufacturer (IDM) model - controlling everything from design to fab - holds an absolute advantage in scale and security, which is exactly what top-tier AI developers are craving.

How do they stack up against AMD and NVIDIA?

NVIDIA continues to flex overwhelming dominance in the AI era. Their Q4 FY2026 earnings (ending January 2026) make Intel's numbers look modest by comparison. NVIDIA's Q4 revenue hit a record $68.13 billion (up 73% YoY). The Data Center segment alone raked in $62.31 billion (up 75% YoY). Even crazier, networking revenue spiked by 263%, fueled by NVLink architecture inside Blackwell super-clusters.

With GAAP gross margins touching 75% (dwarfing Intel's 39.4%) and $34.90 billion in free cash flow in a single quarter, NVIDIA’s pure-play accelerator strategy and CUDA ecosystem are printing money at a rate Intel’s diversified model simply can't touch. Still, there's an ironic silver lining for Team Blue: NVIDIA was forced to select Intel's Xeon 6 as the default host CPU for its massive DGX Rubin NVL8 systems. It proves that no matter how dominant NVIDIA is in GPUs, they still can't completely sever their reliance on the x86 system orchestration architecture that Intel built.

While NVIDIA is running a completely different race, AMD remains the direct, existential threat to Intel. In Q4 2025, AMD reported $10.27 billion in revenue (up 34% YoY). Their Data Center segment set a record at $5.38 billion, actually eclipsing Intel's Q1 2026 DCAI revenue ($5.05 billion). Constant pressure from EPYC processors and Instinct AI GPUs is keeping AMD's momentum strong. But what makes AMD truly terrifying isn't just its growth rate; it's their "market skimming" strategy. According to Q4 2025 data from Mercury Research, while Intel is still the volume king (holding 71.2% of server CPU unit share), AMD is gobbling up 41.3% of the revenue share.

Imagine the server chip market as a cake. Even though Intel is selling way more chips (71.2% of the volume), the vast majority are lower-end, cheaper chips (the dry cake base). AMD, meanwhile, is selling ultra-expensive EPYC chips, skimming the richest frosting off the high-end segment. The result? AMD swallows 41.3% of the market's total revenue, despite shipping significantly fewer units.

What does this tell us? AMD is selling the most expensive silicon, eating up the hyperscaler super-server segment, and effectively pushing Intel down into the budget, low-margin server sandbox. The same dynamic is playing out in the PC space, where AMD has surged to 31.2% revenue share by aggressively targeting gamers and workstation users. On top of that, by using a fabless model and offloading manufacturing to TSMC, AMD keeps its depreciation rate at a breezy 8-9%. In stark contrast, running its own bleeding-edge fabs forces Intel to carry a brutal depreciation burden equal to 21% of its revenue.

However, every cloud has a silver lining. With TSMC suffering from severe advanced packaging (CoWoS) capacity constraints that are bottlenecking both AMD and NVIDIA, Intel Foundry's autonomous model is suddenly a massive weapon. By controlling the entire stack - from fabrication in the US and Europe to packaging in Malaysia - Intel is the only manufacturer capable of total self-sufficiency, completely insulating itself from supply chain ruptures and geopolitical volatility in the Taiwan Strait.

A fabless company is like an architect who draws up house blueprints (AMD, NVIDIA) and then hires a construction contractor (TSMC) to build it. The upside is you save billions on building factories; the downside is you are at the contractor's mercy. Intel is an IDM (Integrated Device Manufacturer). They draw the blueprints and spend billions building their own foundries. While the capital burden is immense, when contractors like TSMC are logjammed with orders, Intel's self-sufficient model becomes a critical advantage for ensuring an uninterrupted supply chain.

Capital structure and the SCIP Ireland buyout

Intel's finance team is aggressively maneuvering capital to simultaneously expand manufacturing footprint while guarding liquidity. Exiting Q1 2026, the company held nearly $32.8 billion in highly liquid assets (including $17.2 billion in cash) against roughly $45 billion in debt.

The biggest headline here was Intel dropping $14.2 billion to buy out Apollo Global Management's 49% stake in Fab 34 (Ireland). To close the deal, Intel deployed $7.7 billion in cash and took on $6.5 billion in short-term debt. The upside of this SCIP (Semiconductor Co-Investment Program) Ireland buyout is glaringly clear: it dismantles the complex legal structures of a Variable Interest Entity (VIE), and terminates expensive milestone penalties tied to construction timelines or minimum volume commitments required by Apollo. Most importantly, it lets Intel keep 100% of the profits. CFO Dave Zinsner dubbed it a "highly accretive" move that will save Intel up to $1.1 billion annually in Non-Controlling Interest (NCI) profit allocations - essentially the profit cut owed to minority shareholders - during the 2027-2028 window.

Legal and geopolitical risks

Intel's Q1 2026 10-Q filing contains stark warnings about macroeconomic risks that could directly threaten the global supply chain.

- The Middle East: The Israel-Iran conflict poses a direct threat to Fab 28, a crucial Intel manufacturing hub in Israel. The critical vulnerability here is that traditional property insurance doesn't cover acts of war, terrorism, or political violence, forcing Intel to be largely self-insured. Any physical incident at this facility would sever the global CPU supply.

- The Helium Crisis: Iranian attacks on Qatar have triggered a shortage of helium, a vital cooling gas used in wafer etching processes. Record-high material costs forced Intel into emergency price hikes during Q1 just to protect its margins.

- Billion-Dollar Litigation Pressures: On the legal front, Intel is carrying a $1 billion liability provision for a patent infringement lawsuit with VLSI in Texas. On top of that is a $310 million provision for a relentless antitrust fine from the European Commission (EC) dating all the way back to 2009. Although the General Court reduced the base amount to 237 million Euros in December 2025, Intel continues to appeal to the EU Court of Justice in early 2026.

The bottom line

Wrapping up, the Q1 2026 earnings report doesn't paint a rosy picture of an undisputed king reigning from the mountaintop. Rather, it reads like a promising discharge paper for a seasoned veteran recovering from massive reconstructive surgery. The lingering scars of past sluggishness are still visible, compounded by the relentless pressure from archrival AMD, the colossal shadow of NVIDIA, and a minefield of geopolitical variables.

Still, thanks to the ironclad discipline of the executive team, a node roadmap that is actually hitting its targets (especially the 14A process), and the rising tide of Agentic AI workloads, Intel has found its most authentic and promising growth momentum in half a decade. The Intel narrative is no longer a story of pure survival; it has officially shifted to the scale-up phase, sprinting to catch the high-speed train of the AI era.

Brace yourself for shortages and price hikes on the new Core Ultra lineup through at least the first half of 2026. The AI PC boom, colliding with hard manufacturing constraints (like substrate and memory limits), means Intel simply cannot build them fast enough to meet demand. Furthermore, if you see screaming headlines about Intel's $4 billion loss, take a breath and recognize it as an accounting maneuver (tied to Mobileye); Intel's core silicon manufacturing business is actually mounting a very aggressive comeback anchored by the 14A node.